Over the past two decades, while the Reserve Bank of India (RBI) gave out licences to set up universal banks, small finance banks and payments banks to increase banking penetration in the country, it stopped altogether issuing licences for urban co-operative banks (UCBs).

The reasons for the RBI’s reluctance are not far to seek. After the liberalisation of licensing norms in May 1993, until June 2001 it had issued 823 licences for UCBs. But due to lack of good governance, nearly a third of these newly licensed banks became financially unsound within a short period.

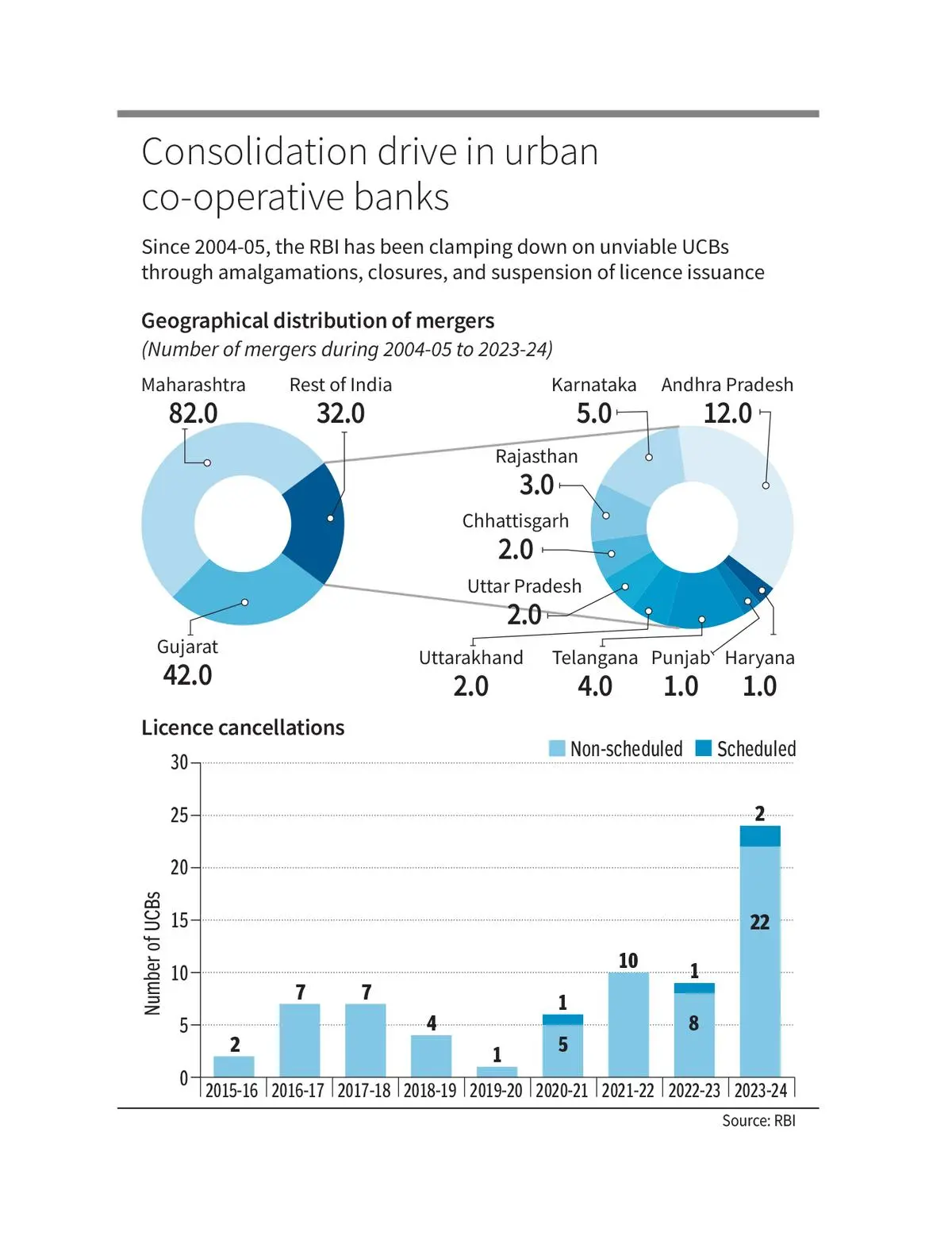

Naturally, the RBI slammed the brakes on new licences for the UCB sector. Starting FY2005, the central bank initiated a process of consolidation, including amalgamation of unviable UCBs with viable counterparts and closures, according to its latest Report on Trend and Progress of Banking in India.

The number of UCBs declined steadily over the last two decades — from 1,926 to 1,472.

But now, with the NDA government seeking to make the cooperative movement a mass movement (‘Sahkar se samriddhi’, or progress through cooperation) for the development of the country, Union Home and Cooperation Minister Amit Shah wants a UCB in every city.

In early March 2024, at the inauguration of the umbrella organisation for UCBs — the National Urban Cooperative Finance and Development Corporation (NUCFDC), Shah underscored the need for UCBs to upgrade (people, processes and technology) and adhere to RBI regulations.

Task force

UCBs are member-driven and community-based banks operating in urban and semi-urban areas. Their focus is on lending to micro, small and medium enterprises (MSMEs), weaker sections, retail (housing, education, and so on), and agriculture and allied activities.

Given that the UCB sector is in the midst of consolidation, is the time ripe for opening it up for new licences?

Cooperative banking sector experts say the RBI may either wait until the number of unviable banks declines or allow the conversion a few large multi-State cooperative credit societies into UCBs.

An indication of the financial health of the cooperative banking sector, including UCBs, and district, central and state cooperative banks, comes from the deposit insurance claims settled by the Deposit Insurance and Credit Guarantee Corporation (DICGC).

In FY24, co-operative banks accounted for the entire deposit insurance claims, amounting to ₹1,436.92 crore (₹751.78 crore in FY23), settled by the DICGC: ₹175.71 crore pertained to claims of liquidated and merged banks; and ₹1,261.21 crore pertained to banks brought under all-inclusive directions (AID).

To revitalise the sector, the National Federation of Urban Cooperative Banks and Credit Societies (NAFCUB) has set up a task force on ‘transformation of UCBs and credit societies’.

Need for norms

D Krishna, former chief executive of NAFCUB and head of the task force, says one of the terms of reference is ensuring that UCBs are spread evenly across the country, so that every urban centre has an urban bank. Currently, UCBs are concentrated in Maharashtra, Gujarat, Karnataka, Andhra Pradesh, Telangana and Tamil Nadu.

Further, the task force will examine whether large co-operative credit societies, especially multi-State, can be converted into UCBs.

Krishna points out that the Ministry of Cooperation has done some initial spade work by issuing prudential norms for multi-State co-operative credit societies.

The Central Registrar of Cooperative Societies has issued the prudential norms, prescribing liquidity, exposure, and other norms relating to capital, capital adequacy ratio, and so on, and branch expansion.

Jyotindra Mehta, Director, NAFCUB, says: “The problem is that we (UCBs) are sitting in our own kingdoms. We don’t look outside it. And most of our banks have remained small for many years.

“We should grow... take every small and mid-sized UCB from one tier to the next. In addition, we should double our profits in the next five years.”

In India, there are 850 UCBs classified as tier-I (with deposits up to ₹100 crore); 538 tier-II (above ₹100 crore and up to ₹1,000 crore); 78 tier-III (above ₹1,000 crore and up to ₹10,000 crore); and six tier-IV (above ₹10,000 crore).

Spreading wings

During 2023-24, the consolidated balance sheet of UCBs exhibited muted growth of 4 per cent, albeit higher than 2.3 per cent in the previous year, as per the RBI report.

The balance sheet size of UCBs relative to scheduled commercial banks (SCBs) fell for the seventh successive year to 2.5 per cent at end-March 2024 from 3.8 per cent at end-March 2017, dragged down by subdued deposit growth on the liabilities side and loans on the asset side.

Mehta stresses that the collective goal of the UCB sector is to double its balance sheet size relative to SCBs to 5 per cent by 2030 and 10 per cent by 2047.

“There are 400 banks in India which have completed 100 years... So we have to plan for the next 100 years,” he says.

Krishna notes that of the 783 districts in India, about 250 don’t have a UCB. Once set up there, they must earn depositors’ trust through good governance, robust risk management, use of latest IT infrastructure, and well-trained staff.

While stakeholders in the cooperative banking sector, including the Ministry of Cooperation and NAFCUB, are keen that UCBs should spread their wings across the country, it remains to be seen if the RBI shares their enthusiasm.

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.